Anzeige der Artikel nach Schlagwörtern: Eurokrise

Eurokrise Update 2016 nach der EZB Zinsentscheidung, Innovation=Wachstum und Ausblick

Das Videointerview beantwortet wichtige Fragen zu der aktuellen Situation in der Eurokrise.

Die letzte EZB-Zinsentscheidung, die Nullzins und Negativzins Politik beizubehalten und das private Anleihenkaufprogramm zu starten, hat in Deutschland wieder für viel Kritik geführt.

Dies aus der Politik, z.B. in der Person von Dr. Schäuble, der lt. Presseberichten sogar die Nullzinspolitik für das Erstarken der AfD verantwortlich macht.

Aber auch viele Volkswirte stimmten in die Kritik ein, insbesondere am Anleihenkaufprogramm. Auch Peter Bofinger, bis jetzt eher nicht im Lager der EZB-Kritiker meinte, das Ende der Wirkung dieser Geldpolitik sei erreicht. Dabei wird aber die Situation im Euroraum, die nach wie vor defaltionär ist übersehen.

Dieses Interview, greift die Fragen auf und gibt einen Einschätzung. Die Fragen sind:

in conversation with ... Didier Richter BIL #Fintech #Banking #Digital Disruption

The impact of digitalization is felt everywhere, also in traditional banking. Fintech is the buzzword under which many promise the revolution of how we deal with our money and investments and do payments.

But are traditional banks easily disrupted as they deal with data and especially regulation since a long time?

The interview with Didier Richter,

Why the Euro crisis continues, Germany and German banks are at risk and the link to innovation and Startups Update 102015

Iceventure received a couple of questions over the summer concerning the analysis of the Euro crisis and the coverage of Greece.

In particular, three critiques have been formulated:

a) Why continue to keep the Euro crisis on the radar as even the "rebellious" Greek Prime Minister Tsipras committed on the mainstream Euro politics and reform agenda and all have only to work on agreed solutions?

a) Why continue to keep the Euro crisis on the radar as even the "rebellious" Greek Prime Minister Tsipras committed on the mainstream Euro politics and reform agenda and all have only to work on agreed solutions?

b) Why such an appealingly tough stance on Germany as it is one of the best performing countries in the Eurozone especially with the start-up revolution finally also taking place here?

c) Why combining the Euro crisis with innovation and start-ups?

This post is only providing short answers as we are preparing, based on business intelligence work for customers, an updated analysis on the Euro crisis after the new Greek agreement.

Still I deem it important to provide some general comments prior, as we find the main thesis of a major structural change more and more confirmed.

Greece has its part, but is only a puzzle piece in the Euro crisis

First, even with this summer's Greek agreement I do not find any of the Euro issues as a currency area fixed. It is still a dysfunctional currency area with the ECB taking over a political role and a reform debate towards federalism starting only now.

This is the second dominating issue and from market view and realities years away in terms of speed of crucial reforms (as outlined here). Albeit Greece has its role and one can illustrate many Eurozone issues exemplarily, the bigger picture did not change. This issue will stay on the table even with a Grexit which likelihood did not significantly change with the new agreement.

In the meantime, it is interesting to use OCA theory for analysis and compare the Eurozone to the U.S., but we should treat the Euro as it is without the reforms: It is a fixed currency regime either turning into a currency area or falling apart.

Then, as I continue to argue, we deal not primarily with a currency crisis, but with a profound government debt and banking crisis that is amplified in an ill constructed currency area.

The core of the Euro crisis is a government bond and banking crisis in times of secular change

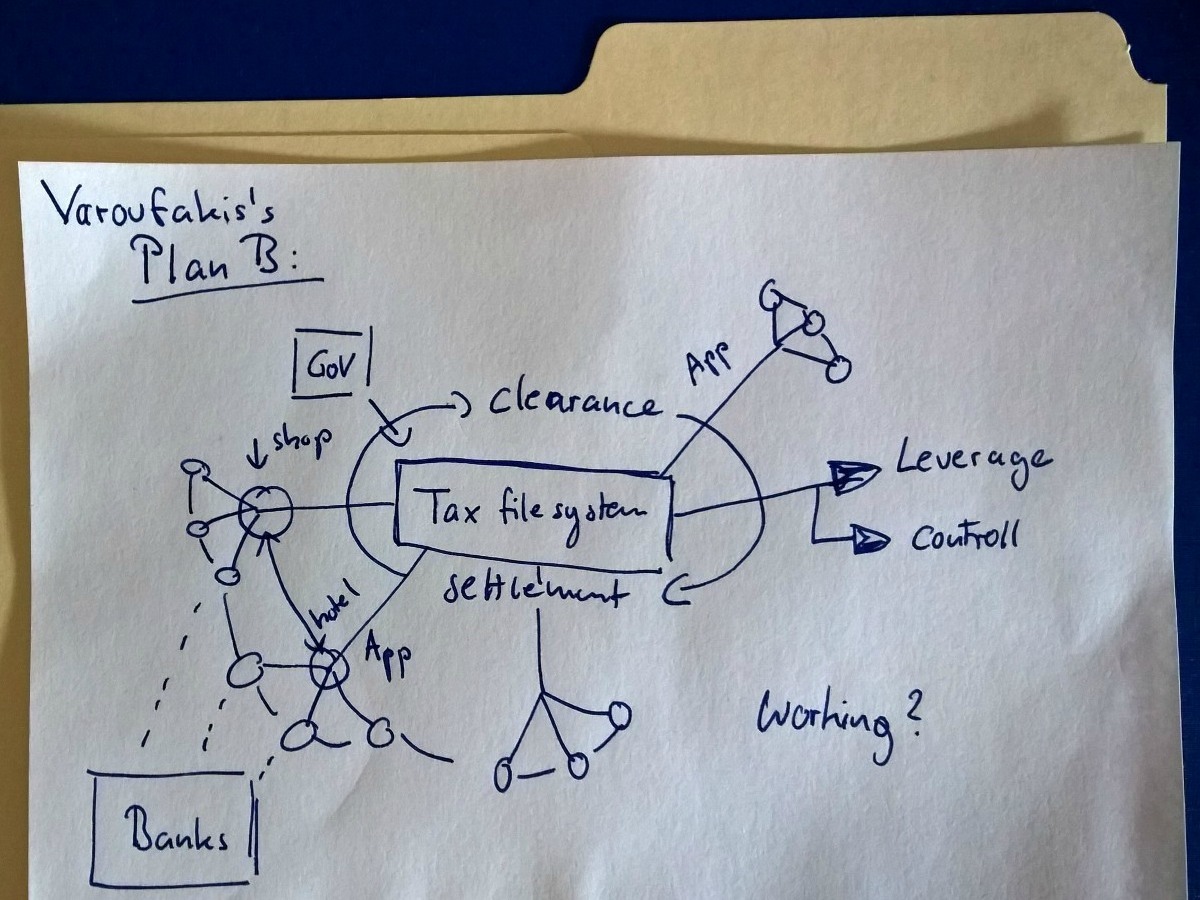

Varoufakis's Plan B provides many Fintech startups lessons and was good

Last week's leak of Ex-FinMin Varoufakis's Plan B to extend the software around the tax numbers of Greek citizens to establish a payment system lead to an uproar in international and German media. General tenor was that once again there was another proof of the amateurishness of the Greek ex finance minister.

However, is this true, just because Plan B is unconventional and outside of everyday perception? My four words answer is: No, it is not.

I will explain my judgment with the analogy of Fintech start-ups, as it is very fitting as Fintech start-ups in this sector (payment) face the same challenges and it makes the argumentation more accessible for readers. It is not to mask or deny the seriousness of Greek's overall situation. It only shows the systematic approache needed and what bad and good sides it had to start with tax numbers and tax software. I also assume an inner Greek system alone, as capital controlls are in place and all external routing has to go via the central bank only. Since the "leaked" tape did not include all details the elaboration and assessment is based on the reasonings why to start with the tax software.

It is also just a perfect example - in line with Iceventure's credo, as our customers know - that new business opportunities build around not only technology, but also cracks introduced by sociological and political change as well action.

When you think of Plan B with the metaphor of "a payment startup" as we do in our innovation workshops - what is your mission? Work today on something totally out of norm that norm it becomes tomorrow. What are the main obstacles assuming that programming skills are there? It is a short list in the end.

Security (Identity), a functioning process, easy to handle, working (almost) everywhere and the liquidity to run it. So let us go through the important points:

1. Safety & Identity verification in payments systems

Idiology vs. reason? A thought experiment about the strategy of MiPr Tsipras and FinMi Varoufakis agains the EU

Note: This piece might be subject to language editing as it is a translation. The German version of the articel is avilable here.

Update 14.07.2015: An interview with Ex-FinMi Varoufakis confirmed a larger part of the strategy laid out. The question is what happened that PiMi Tsipras folded. Post your opinion in the comments.

So many things have been written about the two Greeks. Comments depicting them as incompetent to claiming they are ideologically stubborn. Schulz named MiPr Tsirpas yesterday as "unpredictable". At the moment "capricious" is still the greatest compliment.

Add to this the recent events: A non-paid IMF credit rate, followed by a comment of IMF's Lagarde "to grow up", the introduction of capital controls and bank holidays. Enough reasons for the two actors of the Greek government to be actually deeply concerned and tense, one might presume, because they now face the results of their own "amateur" style politics.

Ideologie versus Vernunft? Ein Gedankenspiel zu MiPr Tsipras und FinMi Varoufakis Strategie gegen die EU

Note: An English version is available here

Updatate 14.07.2015: Ein großer Teil der Strategie wurde inzwischen durch ein Interview des Ex-Finanzminister Varoufakis bestätigt. Frage ist dann, warum Tsipras einknickte.

Was wurde nicht alles über die beiden Griechen geschrieben: Von inkompetent bis ideologisch verbohrt war alles dabei. Schulz sprach heute davon, dass MiPr Tsipras unberechenbar sei. Im Moment ist „wechselhaft" noch das größte Kompliment.

Dazu kommen die aktuellen Ereignisse: das Aussetzen der IMF-Rate, mit der Aufforderung erwachsen zu werden, Kapitalkontrollen und die Schließung der Banken. Alles Gründe für die beiden Hauptakteure der griechischen Regierung eigentlich tief besorgt und angespannt zu sein, da sie nun die Ergebnisse der eigene „Laien"-politk sehen.

Doch die Körpersprache und das Auftreten der beiden Griechen sprechen ganz andere Bände und passen überhaupt nicht zu den Darstellungen, die in Deutschland zu lesen sind. Im Gegenteil - Finanzminister FinMi Varoufakis wirkt entspannt, lächelt. Ministerpräsident MiPr Tsipras wirkt auch nach wie vor sehr ruhig und geht, wenn er öffentlich spricht, zum Angriff über.

Dieses Verhalten ist natürlich Wasser auf den Mühlen der Kritiker, die alle Vorwürfe der Inkompetenz und Unvernunft bestätigt sehen. Doch ist das wirklich so?

Denn nur, weil das Verhalten der beiden griechischen „Helden" nicht den EU-Erwartungen und heutigen Benimm-Normen entspricht, heißt es noch lange nicht, dass die Vorgehensweise nicht geplant ist.

Und musste die EU nicht feststellen, dass MiPr Tsipras von Anfang an einen eigenen Plan verfolgt hatte, immer wieder irritierte und dann alle überraschte als er das Referendum verkündete?

Estimating the costs of a grexit

Information: This is the first part of a longer articel that will be subject to editing. I publish this part immediately as I think people might want to have ideas how to calculate the Grexit costs for Germany and Europe.

Costs of a Grexit for the Eurozone

Costs of a Grexit for the Eurozone

As German and European finance ministers have been more or less silent about the cost of a Grexit, it was once again left to FinMi Varoufakis to speak of one Trillion costs for the global economy.

This is an enormous amount. As it might be an overstated number to get a better deal the question is, is he right? Varoufakis proofed to have sharp analytics, beyond the dream of the EU that spent their time watching the middle finger instead on analyzing his speeches (see Hart aber Fair 29.09.2015 and this article in contrast).

The only studies containing numbers I knew speak about a smaller sums. Today then, first estimates appeared in the wider German press (the Welt) basing their article exactly on these two public available studies by S&P and by IFO. As the Welt limits their indications mainly to an reproduction, I will use both of them here and in addition a 2011 UBS study, but add an in depth analysis around it.

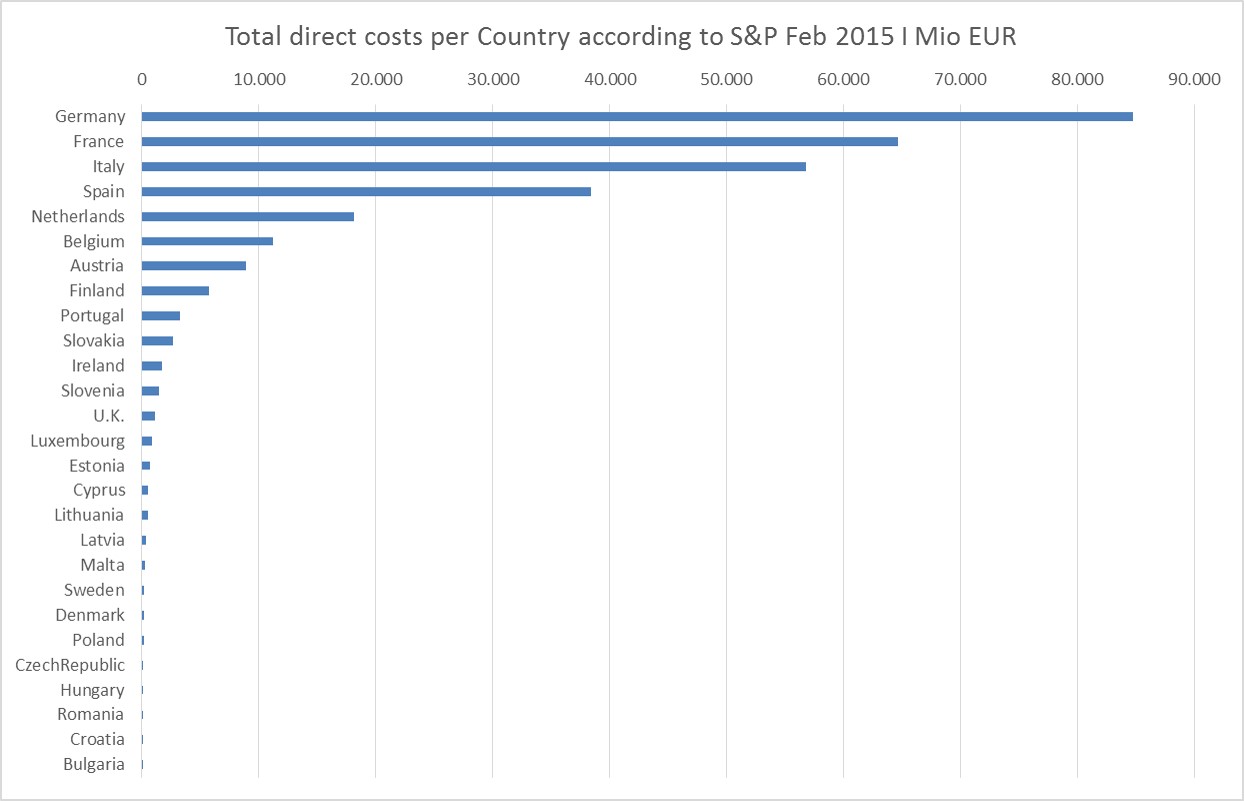

Direct Economic costs

The S&P study contains numbers for all European countries involved, IFO only for Germany. It states €75 - €77 BN costs for Germany while S&P estimates direct costs to € 300 BN in Europe and € 84 BN for Germany. The Welt slightly differs

with in their own calculations.

The UBS study from 2011 arrives at about 80 BN for Germany, thus it seems to be a reasonable estimate. On average this means 3% loss measured in GDP for Europe.

In my opinion this is a substantial loss as it translates to one year of GDP in good times and up to 3 years of GDP when one takes per annum growth in Europe after 2010.

This are so far the known estimates of the direct costs.

However I think it is only reasonable to apply lessons learned from financial markets in 2008 and follow the analytical thinking to estimate the total real costs that also comprise necessary adoptions and the risk/the manifestation of contagion.

Wrap Up zur Eurokrise Verhandlungen Griechenland - EU 062015

Das Videointerview beantwortet wichtige Fragen zu der aktuellen Griechenlandkrise und den Verhandlungen mit der EU aus gegebenem Anlass des Countdowns.

In der zweiten Frage wird dargelegt, warum das große Bild großen Einfluss auf die aktuellen Verhandlungen hat. Wieso ist die griechische Position so stark? Um was geht es wirklich? volkswirtschaftliche Reformen und Wachstum oder

In den folgenden Fragen geht es um die Bewertung und Einordnung des #Grexit, die notwendigen Reformen in Griechenland sowie die Bewertung und Einschätzung des Ausgangs der Verhandlungen mit der EU und der #Troika.

Zum Abschluss werden die Möglichkeiten behandelt, mit Innovation und Start-ups mehr Wachstum zu generieren, um damit die Krise in Griechenland zu beenden.

Digital disruption - the example of the most underrated Fintech startups Tradeshift

I have been working on a Fintech overview project recently. It is quite interesting to see the momentum in this sector with all its remarkable companies and concepts. However, to my surprise, one company I have been following since a couple of years is hardly ever mentioned. I think this is strange given its potential. Therefore, this blog post is about one of the most interesting startups in this sector – Tradeshift. It seems mostly overlooked and to be the most underrated startup in the European if not the global startup scene.

Furthermore Tradeshift perfectly illustrates Iceventure's hypothesis regarding the adaption channel of many internet innovations. We, in contrast to many, think it happens via enterprise tech and not via the consumer tech adaption channel.

In order to explain the case mentioned above, let us proceed step by step, by starting with a quick check of the big picture, followed by a description of the basic services and the main arguments.

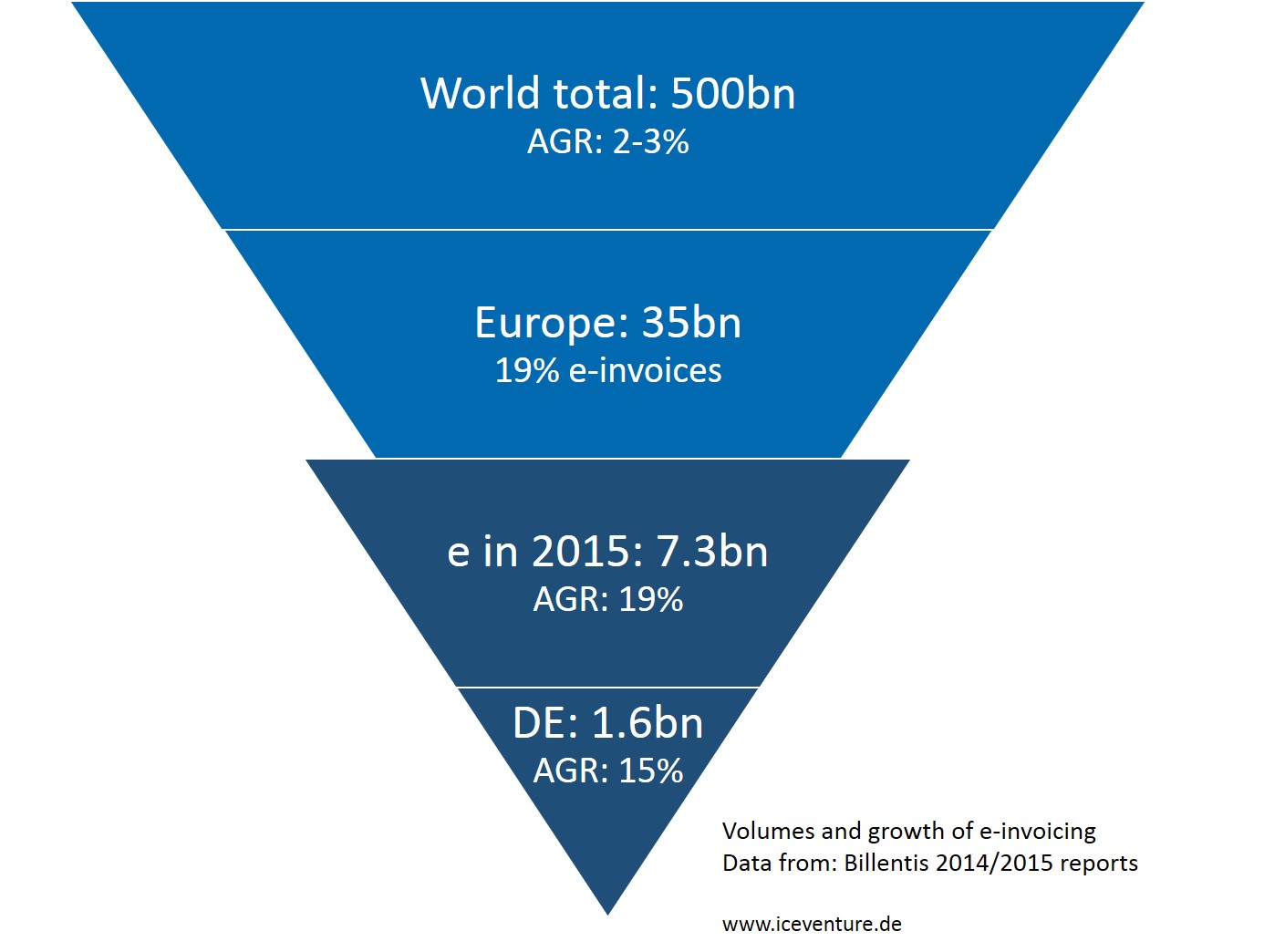

Market size and potential of E-billing

According to a study the annual bill & invoicing volume in the world is at 500bn with an annual growth of something like 2%-3%. Broken down to Europe the amount is estimated to be at 35bn, roughly divided 50:50 between consumer and business (including business to government). In Europe on average 19% of this volume is considered to be transmitted electronically. The market size for E-billing, a further digitalization of this process, is estimated to reach 7,3bn in 2015 with an annual growth rate of 19% (average – B2B/B2G growth is faster than B2C)1. For Germany for example the volume is said to be at 1.6bn with a growth rate of 15,4%2. Numbers for Italy are currently unavailable.

According to a study the annual bill & invoicing volume in the world is at 500bn with an annual growth of something like 2%-3%. Broken down to Europe the amount is estimated to be at 35bn, roughly divided 50:50 between consumer and business (including business to government). In Europe on average 19% of this volume is considered to be transmitted electronically. The market size for E-billing, a further digitalization of this process, is estimated to reach 7,3bn in 2015 with an annual growth rate of 19% (average – B2B/B2G growth is faster than B2C)1. For Germany for example the volume is said to be at 1.6bn with a growth rate of 15,4%2. Numbers for Italy are currently unavailable.

Thus, we are talking about an enormous market volume ready for disruption. That is what Tradeshift aims to do.

Die nächste Zäsur in der Eurokrise – Griechenland vs. EU Update 032015

Info: Der Post wurde am 20.03. mit einigen Fußnoten und kurzen Erläuterungen upgedated, am 21.03. mit einer Ergänzung zu dem auch hier benutzten Video von FM Varoufakis nach der dt. Diskussion (in kursiv).

Nach großem Hin und Her und viel Theatralik, kam es am Dienstag vorletzter Woche zu einer Einigung zwischen Athen und den EU-Institutionen. Nachdem durch die Vorgänge bis zur Einigung die Diskussion um den Euro-Raum neu angefacht wurde, ist es wichtig, diese neue Situation und die zukünftigen Auswirkungen auf die wirtschaftlichen Entwicklungen in der EU vertieft zu analysieren. Denn die Entwicklungen, die sich um den Fall Griechenland ergeben, stellen eine weitere Zäsur in der Eurokrise dar.

Die Analyse erfolgt entlang von den drei dominanten Fragen in der öffentlichen Diskussion in Deutschland. Diese wurden uns auch nach dem letzter Artikel zur Eurokrise und den Verhandlungen von Griechenland vs. EU in hitzigen Diskussionen und E-Mails gestellt. Eine Überprüfung dieser Fragen führt folglich hervorragend durch die Situation. Sie bieten auch den Hintergrund für die deutliche abweichende Bewertung der Ergebnisse und Situation von meiner Seite. Diese sind:

Die Analyse erfolgt entlang von den drei dominanten Fragen in der öffentlichen Diskussion in Deutschland. Diese wurden uns auch nach dem letzter Artikel zur Eurokrise und den Verhandlungen von Griechenland vs. EU in hitzigen Diskussionen und E-Mails gestellt. Eine Überprüfung dieser Fragen führt folglich hervorragend durch die Situation. Sie bieten auch den Hintergrund für die deutliche abweichende Bewertung der Ergebnisse und Situation von meiner Seite. Diese sind:

• Wichtigkeit der Berücksichtigung der Schuld von Griechenland an der Situation. Ist deswegen die Härte angebracht und es nur legitim, die deutschen und europäischen Interessen so zu vertreten.

• Bewertung der Verhandlungen und Einschätzung zur Verhandlungsmacht der griechischen Regierung. Ist sie wirklich so schwach und eine „Laientruppe"?

• Griechenlands Alternativen ohne die EU

Nach der Beantwortung und Bewertung dieser Fragen, wird argumentiert, dass die Härte und der Ton von Seiten der EU unter deutscher Führung im Gesamtkontext nicht zielführend sind. Es wird dargestellt, dass wir damit vollständig in das Paradigma der Machtpolitik ohne Verankerung wirtschaftlicher Ziele, der nächsten Zäsur in dem Ablauf der Eurokrise, angekommen sind. Dabei wirkt die EU insbesondere vor den aktuellen geopolitischen Veränderungen strategisch ziellos.

Abschließend werden kurz die Folgen für Unternehmen und Innovation dargestellt.