I have been working on a Fintech overview project recently. It is quite interesting to see the momentum in this sector with all its remarkable companies and concepts. However, to my surprise, one company I have been following since a couple of years is hardly ever mentioned. I think this is strange given its potential. Therefore, this blog post is about one of the most interesting startups in this sector – Tradeshift. It seems mostly overlooked and to be the most underrated startup in the European if not the global startup scene.

Furthermore Tradeshift perfectly illustrates Iceventure's hypothesis regarding the adaption channel of many internet innovations. We, in contrast to many, think it happens via enterprise tech and not via the consumer tech adaption channel.

In order to explain the case mentioned above, let us proceed step by step, by starting with a quick check of the big picture, followed by a description of the basic services and the main arguments.

Market size and potential of E-billing

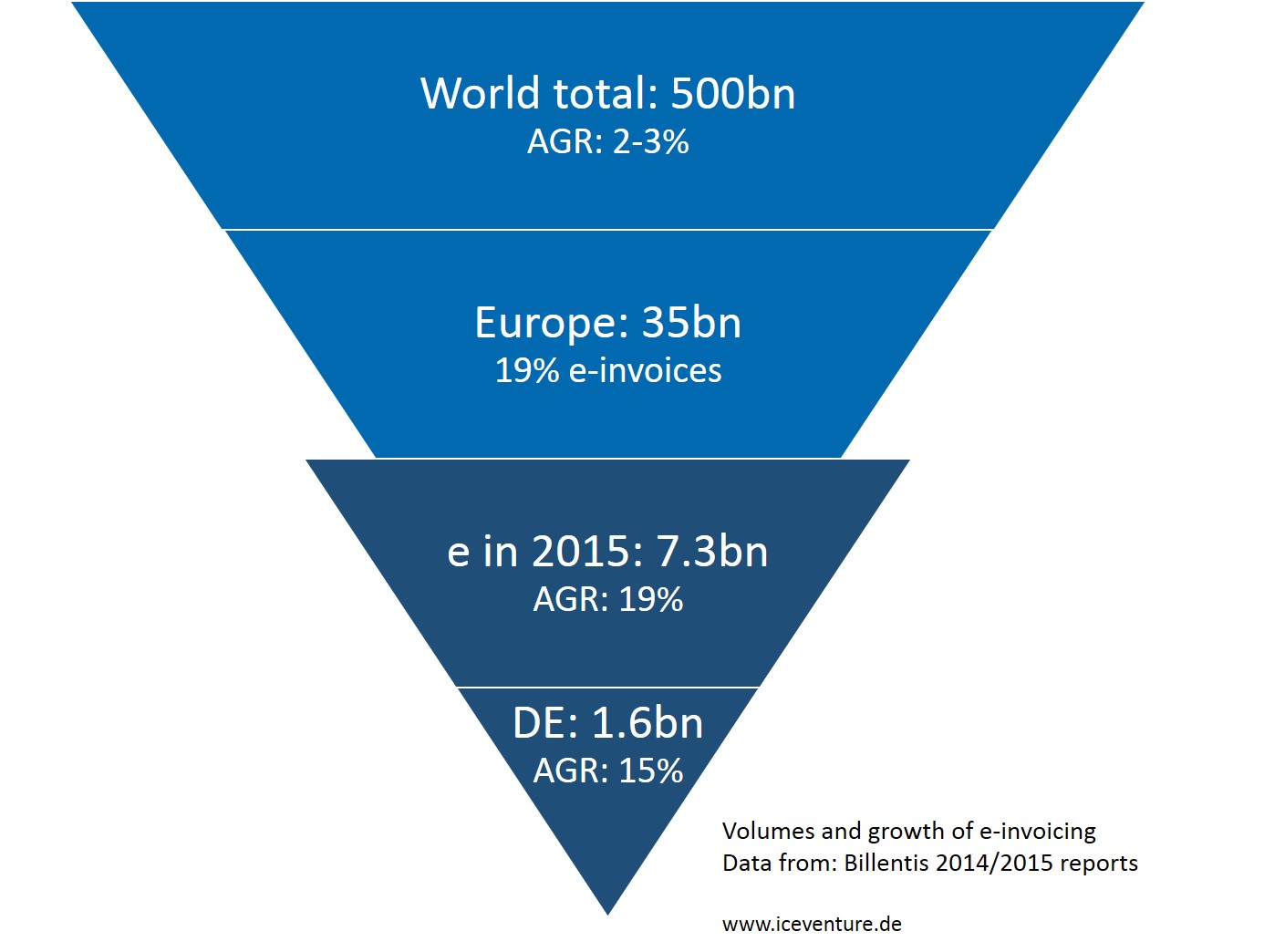

According to a study the annual bill & invoicing volume in the world is at 500bn with an annual growth of something like 2%-3%. Broken down to Europe the amount is estimated to be at 35bn, roughly divided 50:50 between consumer and business (including business to government). In Europe on average 19% of this volume is considered to be transmitted electronically. The market size for E-billing, a further digitalization of this process, is estimated to reach 7,3bn in 2015 with an annual growth rate of 19% (average – B2B/B2G growth is faster than B2C)1. For Germany for example the volume is said to be at 1.6bn with a growth rate of 15,4%2. Numbers for Italy are currently unavailable.

According to a study the annual bill & invoicing volume in the world is at 500bn with an annual growth of something like 2%-3%. Broken down to Europe the amount is estimated to be at 35bn, roughly divided 50:50 between consumer and business (including business to government). In Europe on average 19% of this volume is considered to be transmitted electronically. The market size for E-billing, a further digitalization of this process, is estimated to reach 7,3bn in 2015 with an annual growth rate of 19% (average – B2B/B2G growth is faster than B2C)1. For Germany for example the volume is said to be at 1.6bn with a growth rate of 15,4%2. Numbers for Italy are currently unavailable.

Thus, we are talking about an enormous market volume ready for disruption. That is what Tradeshift aims to do.

Tradeshift - Services and features

Tradeshift is a global online platform for e-billing present in 150 countries. It gives its customers a neat and nice way of editing and sending invoices to the purchaser. The recipient then can quickly check the invoice either manually or by means of automated business rules. Moreover they can give feedback, ask for changes or send back the invoice altogether. For suppliers this means free electronic invoicing, faster payments, and a more predictable cash flow.

Enterprise customers can collaborate more easily and productively with their entire supply chain, anywhere in the world. In order to make work easier and more productive, there is both an ERP integration and a service for digitalizing documents called CloudScan.

This is only the first layer of services. Of course, the full cycle of procure to pay is easily manageable. The handy features of the platform provided by Tradeshift also allow companies to enable and to control financing of the supply chain. Once connected with many, if not all, your suppliers on a common platform, you can organize the full supply chain and supply chain financing programs as well as dynamic discounting very easily.

But that's not all: Tradeshift also offers third-party integration, an API and a kind of app market, which I will explore in the next paragraph.

They thought about an ecosystem and an API, too - the root for Fintech disruption

Tradeshift thought about an app market for external developers from the very beginning. It however seems that too few seized the opportunity for the offer is no longer directly available on their website. Nonetheless, the more than kind Senior Global Communications Manager Peter Adams told Iceventure via email that Tradeshift still welcomes external projects interacting with them in two ways: "There's the development platform to build apps, and Tradeshift Studio where we work with customers on conceptualization and design ourselves."

An opportunity for digital disruption of processes with a full ecosystem

This is remarkable for third party developers that are offered an opportunity to

a) Get indirect access to financial data as basic ingredient for any kind of visualization (such as dashboards) or business workflows and processes

b) Through this access, they can disrupt ERP software on a large scale.

c) Through this access, one can disrupt financing on a large scale

This in my opinion holds especially true for service offers in that area for SMEs that have difficulties to stem the investment in an independent EPR system to this date. Add to this the setup costs of establishing or participating in a supply chain finance program and all controll mechanisms that now become possible. Modularized apps based on the key financial information automating some tasks e.g. with links to tax authorities could change the game. They could also cut out some of the classical consultants (tax advisors, bookkeepers) doing the work for SMEs and often have high costs.

In addition, outside collaboration could also extend to providers of financing solutions or metric providers. Some partnerships between Tradeshift and other companies in that area are in place, but I think that there is plenty of room for more.

Current valuation and backing of the startup Tradeshift

With all that, Tradshift got great support by outstanding people like Morton Lund who even served some time as the chairperson of the company. Stefan Glaenzer is also on board. The latest financing round was in Feb. 2014, bringing in an additional $75m at an above $ 300m valuation. According to Crunchbase, another round of $30m followed in May 20143. The company claims to process $10bn of annual transactions4.

To sum it up: The data and features sound good. But does it hold true to the initial claim? In the end, e-invoicing is or will quickly become a commodity and there are many competitors in the billing sector. All factors not necessarily good for business and valuations. I still think so as the potential of Tradeshift is beyond the visible. Let me explain:

The unlocked Unicorn potential

It´s my conviction that when great companies meet macro trends they become rockets. In the case of Tradeshift, this could become true. Because once you have the e-invoicing platform as a basic layer, many other value services are possible. The arguments for this claim are as follows:

A new era of payment and of supply chain financing

Firstly, with Tradeshift's platform it is possible to offer trade finance services, the oldest form of merchant banking. Credit against documents - but in real time. This is possible on two levels. E.g., a large buyer could offer it within its own supply chain not only via discounts, but also via access to funds.

In addition, also outside creditors could be offered access to a predefined batch of invoices accustomed with analytics and a risk profile. This is stunning for closed credit funds for instance or other investors willing to underwrite risk. They are offered a wide sample (wider than the sample of any company's principal bank) of risks to invest in, either in quantity or quality facilitating layering of structured finance (sector wise/risk profile wise) the easy way. This takes a lot of pain away from companies and investors.

Secondly - you might be tired of talking or hearing of it - but currently we have the biggest financial crisis of the last 70 years ongoing in Europe. The key problems are the recapitalization of European banks and government debt.

Now you might ask: How is that connected to invoicing? Well, receiving and sending money to pay bills is part of the payment system offered by banks mixed with their financing by deposits. This means, if one goes down as well does the payments system, as companies cannot access their money to pay bills.

Payments without banks

The interesting side effect of Tradshift is that it can solve the payment issue, too:

a) It could easily turn into some kind of clearing house for invoices. This means that all invoices exchanged via Tradshift could be netted. Do not laugh, but the Russians had a similar mechanism for invoices in the cold war days which was pretty effective. And in financial markets clearing houses are well known.

b) Add to that a payment function that has some features of Bitcoins (these features are the interesting parts of Bitcoins while the currency pitch is awful! So beware, but the details here are for another post). This means 1:1 encrypted and secure exchange of payments, inbuilt in the platform or offered by a third party. Here we have the enterprise channel adaption of tech. The argument will be picked up in the closing paragraph of the article.

In other words, the accumulated meta data about invoicing offer Tradeshift and its ecosystem partners many options and opportunities to offer additional business driven services. The management of Tradeshift can thus simply decide what to execute themselves or - in case it is not a core competency – pass it on to qualified third parties against a fee.

With the additional services in place it can also help to solve systemic issues. As it might sound a bit abstract for many readers, I will explain the overall benefits with one example.

The potential of Tradeshift illustrated with the Italian example

I will shortly illustrate how well all these features play out together with the example of Italy and Italian companies. The arguments in general are probably valid for many EU countries. Italy, however, is a very suitable example as many companies are lacking behind with digitalization. Furthermore the Italian government made e-invoicing obligatory for their contractors. After a trial period, it became mandatory in 2015. A company called Sogei spa runs their system, a state owned company. So there is a natural trigger introduced by regulation and a most likely solution not driven by competition and user's needs. In addition, there are particular economic problems in Italy stemming from systemic issues in particular manifesting in the current crisis.

Issuance of invoices and long payment cycles

There are typical long payment cycles in Italy. In fact, an invoice circle in Italy takes about two months, not to speak of payments to be made by public contractees. Add to that payments being late (2012: on average 40-50%) and the cycle goes three month.

Cost of data preparation for invoices, decision making and taxes

As many small and medium sized companies are lacking behind with softwarization and digitalization they have to rely on external providers. Costs of course vary, but to cite one example, the chairman of lvh, an association of small companies and freelancers in Alto Adige, a Northern region in Italy speaks of 15-50 Euros per invoice.

Then there is the profession of "comercialista" a kind of auditor, tax and business consultant in one person. As most small companies do not have the time (or knowledge) for bookkeeping, they entrust one of these consultants with this task. Most of the time it is about copying invoice data back into another system. However, this comes also at a hefty price tag.

Here a solution like Tradeshift and third parties apps have a huge potential.

Lack of data, KPIs and dashboards

As a direct consequence of the point above one can imagine that important data and overviews for decision making in SMEs are often lacking or take extra effort to obtain. In fact, based on own consulting experience there, the reason for company problems are often missing up to date information about cash flows. As the costs in terms of investment and time to curate for tools is high for SMEs, there is plenty of room for easy and quick solutions.

The financing gap

Obtaining funds for SMEs in Italy has always been difficult. Ever since the start of the Euro crisis, Italian companies have been facing a credit crunch, obviously making the difficulties worse. The structural aspect of many small/medium companies does reinforce the effect, as they do not have a large balance sheet to finance themselves.

I think it is self-evident that the Tradeshift platform leveraged with the help of (Italian) entrepreneurs as third party developers can help to solve all three problems. Together these are very handsome features and opportunities as not only the pain of billing becomes easier. With the platform and API at hand, it could be finally possible to have better and more real time financial data for the management. Moreover, it could be possible to cut off the payment function from banks entirely. This is a double win as it lowers transaction costs as well as administrative and financing costs and provides much needed funds.

Thus, it is the combination of advantages on each service level for individual players (management, companies, investors, regulators) enabled by this platform which in my oppinion make the case such compelling. Although, there is a big picture, it is brought about by individual actions.

The systemic feature of platforms like Tradeshift for financing and banking

But, the last piece of the puzzle for the disruptive claim and unicorn potential is to transport the problem solving for companies on a more abstract level. Because there are two interesting side aspects.

The first one is the link to tax collection. Tax evasion is often a problem, with negative effects for honest companies. Thus, this solution could be of major interest for governments. As this holds true in general, I again refer to the Italian example. Tax evaison is a major issue here. As a consultant and knowing how the Italian government works, I have to add that it is important to make sure that governments will use the instrument for tax reforms and not to increase tax pressure on companies further, especially in the case of Italy.

The second aspect of crucial importance: In the current macroeconomic environment organized payments (and financing) without banks could become a cornerstone in keeping the payment system alive when the next wave hits European banks. This feature is a hidden gem and maybe a key driver in Fintech taking away core business from banks. This would be an trigger for change. It is exactly the combination of potentially cheaper processes with a more efficient solution at large. And it is a change that is not introduced by planning or regulation, but by individuals in search of more efficient solutions, the classical case for an innovation spread.

This point is important when we discuss innovation and tech adaption in a secular crisis. I had the opportunity to listen to the presentation by the CEO of a large German bank. He presented an analysis of customer demands, saying that apart from all digital channels clients want to have the personal contact, giving the bank a competitive advantage. I asked about identifying the right adoption channel. Because when companies identify a way to save money, it will drive adaption – a normal path in innovation spread.

Summing it all up, you might now understand why I consider Tradeshift underrated and the untapped third party opportunity huge. In fact, I expect to see the Zynga of Tradeshift eventually emerging soon.

If you want to discuss the article or book my consulting just contact me.

For start-ups we also offer the fast and easy 1-hour Start-up consulting - a digitalized service

Footnotes and References

1) Numbers are taken from the report "E-Invoicing / E-Billing International Market Overview & Forecast" Feb 2014 and Feb 2015 provided by Billentis/Robert Koch (www.billentis.de)

2) The German estimate is derived from the report "Die deutsche Internetwirtschaft 2012-2016" provided by eco – dem Verband der deutschen Internetwirtschaft e.V. authored by Arthur D. Little. http://www.adlittle.de/uploads/tx_extthoughtleadership/2013_Report_TIME_eco_Deutsche_Internetwirtschaft.pdf

3) https://www.crunchbase.com/organization/tradeshift

4) http://www.ft.com/cms/s/0/407bcd88-9e29-11e3-95fe-00144feab7de.html#axzz3VIZHw3OS

5) http://www.lvh.it/de/elektronische-fakturierung-50-euro-pro-rechnung-sind-sehr-wohl-ein-problem

6) https://www.informadb.pt/biblioteca/ficheiros/27_payment_study_2013.pdf

Schreibe einen Kommentar

Achten Sie darauf, die erforderlichen Informationen einzugeben (mit Stern * gekennzeichnet).

HTML-Code ist nicht erlaubt.