Information: This is the first part of a longer articel that will be subject to editing. I publish this part immediately as I think people might want to have ideas how to calculate the Grexit costs for Germany and Europe.

Costs of a Grexit for the Eurozone

Costs of a Grexit for the Eurozone

As German and European finance ministers have been more or less silent about the cost of a Grexit, it was once again left to FinMi Varoufakis to speak of one Trillion costs for the global economy.

This is an enormous amount. As it might be an overstated number to get a better deal the question is, is he right? Varoufakis proofed to have sharp analytics, beyond the dream of the EU that spent their time watching the middle finger instead on analyzing his speeches (see Hart aber Fair 29.09.2015 and this article in contrast).

The only studies containing numbers I knew speak about a smaller sums. Today then, first estimates appeared in the wider German press (the Welt) basing their article exactly on these two public available studies by S&P and by IFO. As the Welt limits their indications mainly to an reproduction, I will use both of them here and in addition a 2011 UBS study, but add an in depth analysis around it.

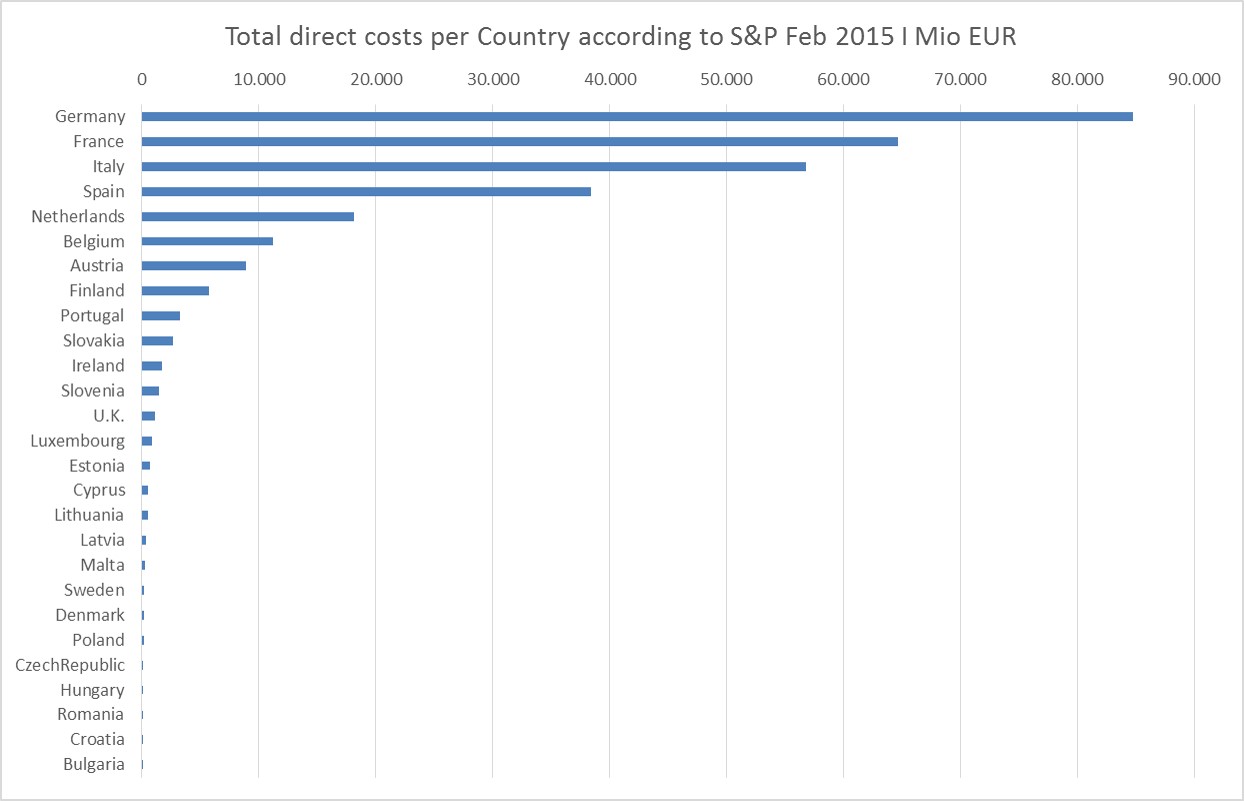

Direct Economic costs

The S&P study contains numbers for all European countries involved, IFO only for Germany. It states €75 - €77 BN costs for Germany while S&P estimates direct costs to € 300 BN in Europe and € 84 BN for Germany. The Welt slightly differs

with in their own calculations.

The UBS study from 2011 arrives at about 80 BN for Germany, thus it seems to be a reasonable estimate. On average this means 3% loss measured in GDP for Europe.

In my opinion this is a substantial loss as it translates to one year of GDP in good times and up to 3 years of GDP when one takes per annum growth in Europe after 2010.

This are so far the known estimates of the direct costs.

However I think it is only reasonable to apply lessons learned from financial markets in 2008 and follow the analytical thinking to estimate the total real costs that also comprise necessary adoptions and the risk/the manifestation of contagion.

Indirect economic costs - what might be the nasty surprises and contagion

In other words, the big unknown remain costs of potential contagion. The dimension of a contagion is difficult to measure and there are time constraints to produce meaningful and reliable numbers. I therefore will only indicate what a hard - nosed family office investment manager might look at using the S&P study and their approach to calculate costs.

In general, a good proxy will be the cost of policy actions necessary to prevent contagion + the costs in case some form of contagion is visible. Prior to going through the S&P study set-up I will indicate two very rough proxy measures.

Contagion risk via the banking system

First, it is the context again. Europe, doing another political mistake during the ill-administrated banking rescue, did not fully recapitalize its banking system yet. Estimates also vary in this respect, but a figure of € 800 BN is in the room. This is reason to worry, but let us assume that the ECB, now being the responsible regulator, is able to solve the issue.

As this means no direct default while most likely a continued transfer of risk to the balance sheet of institutions, a full list of direct economic costs should include remaining exposure not only of German but European banks in order to check for interconnectedness. S&P cites a study of BIS that estimates an exposure of $ 77 BN by banks globally (it is unclear if they meant EU as they then list non EU banks).

But as Greek banks are on the brink and depositors might face a bail-in, one channel of contagion might be a form of soft bank run in other countries. These are likely to appear in countries that are part of an EU program and in which the population is sensitive to the issue: Ireland, Portugal Spain and Italy with a said total deposits of 3.500bn. What would be the number? As currently now reliable estimate is possible, I will only outline the effect: it creates deflation as it means money moving out of the system a trend in place in the Euro anyway ( read a more in detail analysis about deflation and the German misinterpretation of the ECB decision last year here). The ECB would have to provide that money.

Contagion risk from increasing rates

Another contagio risk are widening spreads. Again this is tricky, as the ECB does QE and debt structure changed since 2008. S&P added an update un July 1st stating that spreads are controllable, but will widen for Italy then estimating an additional 11bn on debt serving. Add this to the 61 bn. and you have an increase of 18%. Take this and add the speed with which things change. Remember - in 2008-2010 you could go from hero to zero in days. This also means additional political risk, as the spped does not give time for coordination processes by EU politics.

A qualitative assessment of the S&P study for additional risks

Then the focus is on the items on the balance sheets of the institutions and countries as the major lenders provided in the S&P study. The following questions immediately arise when going through the items step by step:

• Why measure the impact in GDP only?

GDP is helpful for many economic activities and ratios. But in this case national budgets are hit. Thus it makes sense to use them as a reference. German budget is about € 300 BN in 2014. Not a good perspective if you have to take € 84 BN write downs.

Now it is argued that they will not materialize immediately or fully triggered as a cash outflow. I will comment on the cash flows below. But in sum, this might drive up spreads substantially. See the graphic for an impression on the impact.

• What is about optical backstops?

As we learned in 2008, many insurance mechanisms provided by politicians do not stand the test of markets as they are only optical backstops. Where might they be hidden in this list: Take as example the EMS/EFSF. Partially it is paid-in capital, partially there are guarantees. Then the investor's presentations show that government subscribed the same bonds they guaranteed. Sure - one will apply netting to this position, but the complexity and the circular links and references takes time to go through. Time during which investors will be very nervous to find additional unpleasant surprises. And keep in mind political guarantees are in 2015 less credible as markets had to learn in the case of Austrias Hypo Alpe Adria that they might be revoken later as I pointed out here.

Then, what if Greek defaults and callable capital needs to be commited. The very same countries in need of EMS should provide it. This is one of the implicit dangers of an credit guarantee scheme. In case of the Grexit it will work in such a way that countries not longer eligible to provide a guarantee will pass on the burden to other countries. Germany might end up with the most part of it.

This might drive up spreads substantially and/or makes a scenario for soft bank runs more likely.

• possible recapitalization needs of the Eurosystem to be credible

S&P does not consider additional capital necessary. The argument is that e.g. even in case the Eurosystem can take the hit, fear might spread of future events or balance sheet weakness of various institutions. That again triggers a call for additional guarantees and paid in capital in excess of required capital. Someone has to provide it. In consequence public balance sheets further increase with debt.

As readers see this is quite a long list to check for possible contagion and I am sure it is by fare not complete.

This brings me back to the timing of cash flows argument: As national accounting is full of odds, the question is when the loss of e.g. a bond with long maturity not be paid back by Greece will be recorded. As S&P states:

"The largest loss item would likely be the EFSF loans, at approximately €166 billion (...) which official statistics have already included in the general government debt ratio. Standard & Poor's, by contrast, continues to follow its long-standing approach of treating government guarantees for EFSF borrowings as contingent liabilities, not to be included in outright debt (...). Eurozone governments would need to contemplate additional budgetary outlays if and when the guaranteed EFSF borrowings fall due in the future. This impact is important, but will be felt only gradually: Greece is currently scheduled to begin repaying the EFSF program over three decades starting in 2023."

In other words due to the fact that we have to deal with government balance sheets, the write down is only gradually and not based on materialization. Not something that makes an investor really confident as in these turbulent times, budgets might see additional hits in the future.

Interesting is also the handling of S&P of the guarantees for their metrics. Of course financial market professionals know how to deal with that. But under market pressure, there simply might be no time for subtle nuances.

What is about the QE/ECB Draghi put in place?

How to judge about the risks listed above? It is reasonable to assume (or hope) that the ECB and financial institutions learned the points during 2008 to today. Thus there will not be a surprise and QE will mitigate the problems anyway. In other words we now rely on the ECB put with respect to timing and analytical capabilities. Does the Draghi-Put however fully avoid additional costs? I do not think so.

Let us assume that there is no contagion, but due to general uncertainty an on-average cost of 0,5% EU GDP loss could occur. Here another 48 BN Euro go ...

S&P in a recent anouncement, not in the study, speaks about 30bn in 2015 -2015 which means an additional indirect costs of 10% on the direct costs.

To describe the argument to the fullest, I will also dig into the possibility of a lagging risk adoption in a scenario where ECB keeps everything calm and investors have time to think through. Therefore for the pure sake of argumentation I will take a look on a potential alternative translation channel.

An alternative translation channel

As we know form financial crises – they always come as a surprise. Thus it is not enough to concentrate on the known risks. But with ECB in action, what channel might open up?

What when markets – which does not happen to be immediately – come to the conclusion that indeed the ECB with QE can control short term spreads of EU countries. So no reason to speculate here. Then they might figure that the next political move in order to avoid the shock of a second traumatic Grexit like experience is to create even more support mechanisms. The question is then what is the result of the political blame game after the Grexit. Politics will not be able to blame speculators this time and they while blaming Greece to the outside it might not be an option internally, among member states.

In consequence markets might come to the conclusion that the last payer of the Eurozone is or will be Germany! This is exactely the result of the ESM credit guarantees.

Could we then see another move in the German bund including some overshooting as economics teaches us? What new dimension of crisis is that?

This paragraph concludes the section of direct costs.

The "costs" of political decisions framing the Greek negotiations, but independent from them

For an economic analysis, you cannot stop with the Grexit and its associated costs. There was a shift in public narrative since some years, which told (German) public that Greece might be the outlier, the one country not ready for the Eurozone.

In consequence it is said, an exit does not only help Greece, it also makes the left-behind countries and their monetary union stronger. In fact, many economists are arguing in this direction. But does the argument hold true?

The flaws of the Euro remain unchanged with or without a Grexit

Fact is that the remaining Eurozone stays without substantial political initiative what it is today. A gold standard like monetary union with three major flaws against economic logic, but tight into political promises.

Ill-constructed

The Eurozone is ill constructed as member states are not homogenous with respect to their economies and institutional decision making. In additionthere is known common debt (including fiscal powers) whatever you call them And Eurobonds have been excluded by a political decision. Although the EMS and the ECB partly fulfill the same function, it is not sufficient as all the critique of the ECB program shows.

German mercantilist model

As Eurozone countries are tight into a new gold standard with only real prices as an adoption mechanism, the German mercantilist economic model is a problem. It was only Münchau that early argued that the crisis of 2008 in asset prices is rooted in real economy. But did we identify the issue yet?

The point is that prices of other countries do not only have to adjust relatively to be competitive, but also in absolute terms as they have one anchor which is Germany. Germany in order to boost exports as the only measure of success, is not willing to move the prices up. In order to prove the point in a simple way, one can argue that an exit of Germany (=return to DM) would bring an appreciation of said 30% (UBS Study 2011). But understand that the appreciation/devaluation of a currency is the fast moving equivalent of the slow moving real price adoption mechanism. I do not think the Eurozone and other countries did understand the point with repect to "becoming more competitive".

I also want to point to the work by Flassback on wages and productivity in Europe.

Government debt crisis

With all the concentration on Greece, many commentators forget that many European states have debts beyond the own defined limit. The word Eurokrise is used in continuation, but in reality we still have e government debt crisis. The banking rescue – the opposite of liberal policy – lead to a further increase and will most likely bring a structural shift in demand for government titel. I could not identify any sustantial initiative in Europe to adress this issue.

In conclusion: In addition to direct costs and with or without contagion it is obvious that the Eurozone is not irreversible and therefore not save.

Of course it can continue for a long time, but it is simply not attractive for investors as there is always the danger of a crisis and split up.

In consequence, it is only logical to think that markets will demand a risk premium for that which goes beyond simply widening spreads but factor in the new situation.

If this is adding up to 1 trillion – only time will tell.

Additional material:

Eric Dor: The exposure of European countries to Greece

So whose problem is greek debt anyway

Schreibe einen Kommentar

Achten Sie darauf, die erforderlichen Informationen einzugeben (mit Stern * gekennzeichnet).

HTML-Code ist nicht erlaubt.