whether it is a scam or not. I already wrote this article answering questions about the allegations, start up events in general, whether you should go there and how to max out on them. In many talks with Startups during the Web Summit almost all of them agreed on the fact that they were getting something out of the event. TN3 from Germany published some statements by startups about their opinion so I point you to them for some impressions.

What other have also criticized: food prices and the WLAN

For food prices I will cite a Dublin cab driver with probably 30 years business experience talking in general about some complaints by the Web Summit: "spoiled kids have to understand that when demand is high, prices go up. This has been the rule for business and will stay a rule". Maybe this time it is best to listen to the street wise. Sure 20 Euro is a lot for a lunch and lower prices would have been appreciated, but also the menu prices in local pizzerias and pubs did not look much different.

The WLan issue was not as bad as for example the comments here and here reported. I for my part can confirm that the WLAN was weak on Tuesday and went away for about half an hour. I did not notice any major hiccups except being sometimes a bit slow during the rest of the event. Is this something you can blame the organizers for and find it ridiculous for a web event? Yes, but besides event critique I get more out of it to take it as a real life example of current restrictions of digital business models. One thing is the "internet everywhere" vision another the availability reality in the EU (WLan in trains? Internet in Airplanes?). Of course moving to Lisbon in 2016 was a hot issue, too.

But way more important than these points are the complaints and discussions by e.g. other news outlets and some participants about the fact that the Web Summit simply grew too big to be of relevance.

The state of the European Ecosystem and the cycle – is the Web Summit still relevant?

I do not share this opinion. I process the event as a "state as it is description" of the current situation in the (European) ecosystem. I think that the example of the Web Summit 2015 and the sum of the content and startups presented there say and imply a lot about the state of the global innovation and start-up ecosystem and especially about Europe. So let me elaborate this argument and view in the following walking through the participants, presentations and startups.

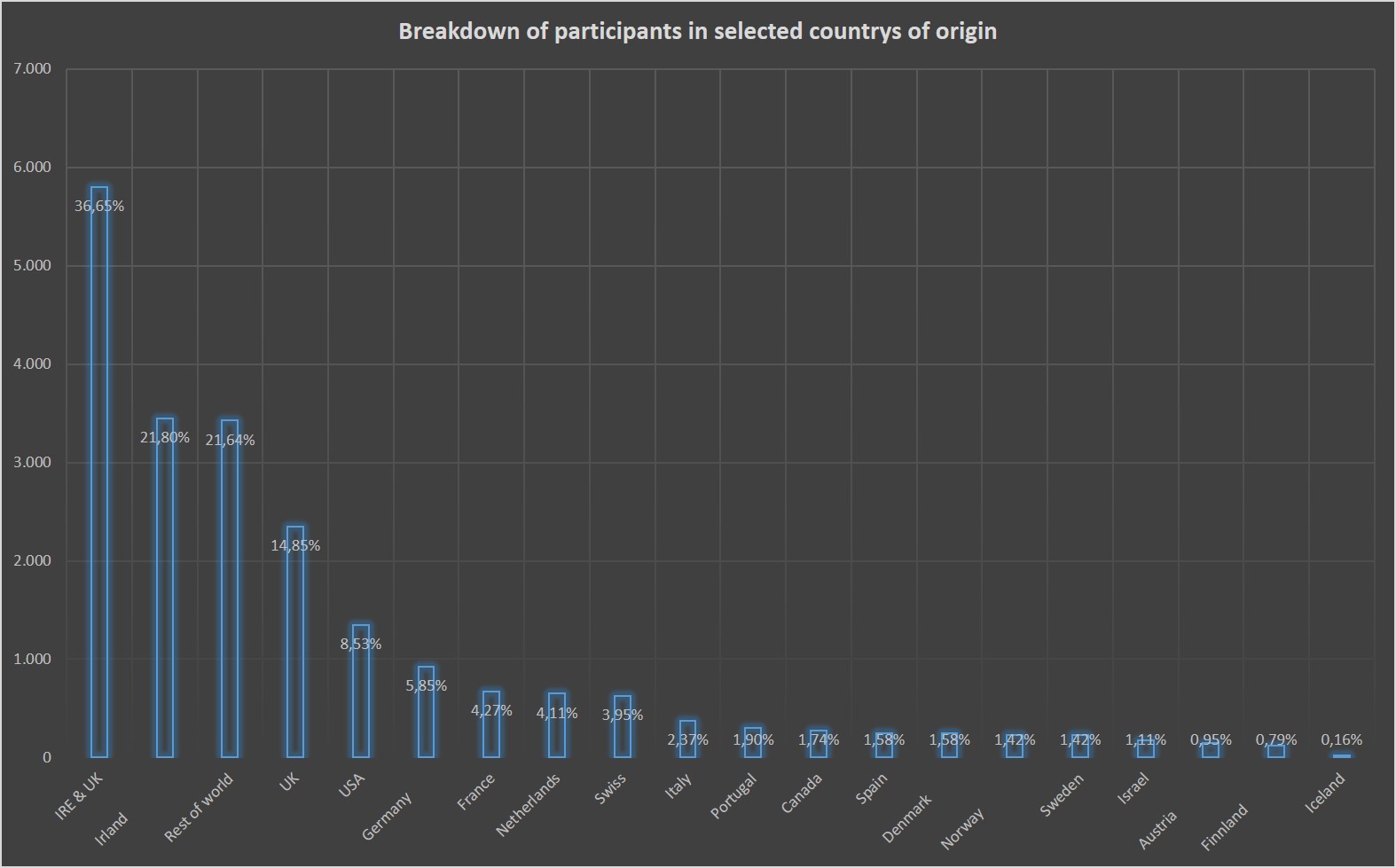

The social Graph of Web Summit participants

To share these insights and argumentation with you let me give you some numbers about the social graph of the participants. Again they have to be taken with a grain of salt as you have a selection bias of conference participation and the numbers include some rounding. The organizers claimed that about 42,000 people participated in Web Summit events at various locations. This is the total number of participants to all events including side events around Web Summit. I stick with the officially announced number of 30,000 tickets sold. About 16,000 of them registered in the official app, which by itself is a kind of interesting factor about the usage of conference technology. But 16k is well enough to have a significant sample.

Here Ireland and UK contribute the highest numbers of participants, in sum 37%. I'm inclined to argue that the number for Ireland is even higher if you check non-app users for nationality. This comes as no surprise since for Ireland and UK it is a home game.

Here Ireland and UK contribute the highest numbers of participants, in sum 37%. I'm inclined to argue that the number for Ireland is even higher if you check non-app users for nationality. This comes as no surprise since for Ireland and UK it is a home game.

The lasting dominance of the U.S. in the start-up field is also confirmed by the fact that the third-place goes to the USA participants with about 9% to 10%. Its dominance is even more significant when looking at the speaker's range. At least felt the US number is about 50% here.

Then we have Germany with 6%, followed by France and Switzerland. The number and % of participation of Switzerland was a bit surprising being a smaller country than Italy which like Canada has around 2% participation rate similar to Denmark. And then of course you have a long tail of countries from all over the world that had a couple of people participating.

This numbers are thus a full confirmation that startups are no longer an exclusive U.S. domain, albeit the Valley trendsetting remains most relevant, but the start-up wave is in full motion also in Europe.

So what about the quality and the business sense of solutions of European start-ups and technology innovation, still questioned by many?

What about the speakers and the presentations

One important factor to determine this aspect and what is really going on in the ecosystem is the content and messages of the presentations. This is for the reason that it provides the context for the current technology and solutions for problems.

And here the Web Summit had a lot to offer. Thousand speakers on several stages, grouped around nine "mini summits" on core topics like Enterprise, Machine, and Data for various subgroups of interest. I agree with other commentators that such a rich program makes it really hard to pick something out. But I cannot say that it was difficult to find something interesting but nothing was really groundbreaking.

For me the most interesting points in the agenda were about "if private data should be an asset class" and about "the future of money", because I think they raised critical question not only about business models but the systemic view that is often shaping developments in a sector long term.

But unlike my fellow commentators I think that these stated concerns and debate about the relevance of the content has less to do with the Web Summit and its organization or its size, but much to do with the current state of the ecosystem and where we are in the cycle. Therefore, it was no surprise to find topics on the agenda like the question for more European unicorns, about mobile first, data in general and how the Internet and its opportunity is going to change and disrupt the world.

In my opinion it can be derived from the content that the major constructs and business model bets on what the future shaped by technology will look like are on the table. And with rising valuations and the typical late movers coming in, we wait for clarification who are the winners and losers. Thanks to the internet and the global promotion of entrepreneurship and start-ups we simply see the main topics amplified all around the globe. I already mentioned the U.S. dominance in the speaker's range. To give you a comparison: I had the opportunity to watch many sessions of Slush in Finland which was a week later. Of course it was different, as it is a different event, different culture with a different approach. But, the main themes and assumptions did not change much.

I think this is a very interesting side aspect of some of the Peter Thiel arguments about globalizing innovation and the American VC model versus real innovating.

As such it was way more insightful to pay attention to side remarks and comments that emerged talking to other participants of which I will list three examples. The first one is about a project that was both – a presentation on stage and side conversation.

The Hyper Loop Project

Talking about Peter Thiel and his thesis I think the most courageous presentation in terms of new concepts and technology was the Hyper Loop project. They try to disrupt public transport and introduce a new high-speed passenger and goods transportation system. My question would've been how they would like to deploy such an innovation as the project resembles very much the German Transrapid that could not be introduced efficiently in Germany or Europe given political and people's resistance. But there was no space for that in the press conference. Once I receive an answer on my follow-up I will share it.

Local VCs and cultural context still important?!

Another interesting example of the side comments was the remark in the press conference by Andreessen Horowitz partner Benedict Evans. In an answer to a lengthy question about China he once again underlined the need for VCs to be local. In his opinion we see even today that VC is still a very local market concept arguing that as a good VC you need close proximity to companies whom you are working with and that culture. This is of course an interesting view with all the debate about the globalization of venture capital and the end of local VCs. And Andreessen Horowitz does not seem to be behind on trends and changes.

IT skills vs. banking risk in Fintech

A third side remark came up in a talk with number26 founder Maximilian Tayenthal. Discussing about Fintech, the event and challenges for start-ups in Berlin/Germany he stressed that they are hiring in order to double their team. Talent is a challenge today. But he also stressed that they are looking for bankers only now "maybe one", being proud that until now there is none. This is of course an interesting comment in the space of Fintech where the risk approach and financial risk taking should be more interwoven into the DNA of the business model than in other sectors. Maybe looking at the backers of number26 explains that easily, but still.

What about great start-ups and business models

The second category and even more important than the speakers are of course the startups themselves. 2141 made their way to Dublin grouped in the major categories, AdTec, Enterprise, Software, Fintech, Social, Travel and e.g. sports.

The status of fundraising seen with Web Summit participants

One indicator to cut through is of course the funding, as money talks. Here, we find another set of interesting numbers. I focused on the top end as the depth and size of rounds is often discussed in Europe compared to the U.S. Of the 2141 startups participating about 100 raised more than 3 million, showing the typical 10% (still nice) selection of investors.

One indicator to cut through is of course the funding, as money talks. Here, we find another set of interesting numbers. I focused on the top end as the depth and size of rounds is often discussed in Europe compared to the U.S. Of the 2141 startups participating about 100 raised more than 3 million, showing the typical 10% (still nice) selection of investors.

Startups from the United States are here again in the lead with 25% members in the "3 mio + club" followed by Germany (14%), UK (13%) and the France (9%). Then follows an interesting list of various countries like Canada (5%), Singapore (4%), India (4%) and Israel (4%).

All these countries already add up to 80% of the club members.

In conclusion the data shows (leaving the US aside) that you can raise significant venture money also in Europe, but this still seems to be locally focused (Berlin/London) and with all the excitement about Europe one should not forget other places (with even more interesting demographics).

The quality improved but the space is crowdy

With this many companies presenting it is impossible to screen or talk to all in detail within three days. However after having talked with at least 50 of them (a good sampling I guess) two major observations come up.

The first observation emerges that on average startups appear to be well prepared. I mean that on average all of them could reasonably well describe the problem they were trying to solve and the next steps in execution and business problems. Knowing the early days of their European ecosystem and the pitches from back then, I think this is a clear improvement.

The second observation is basically in line with the impression about the content. I saw a lot of very interesting and potentially great concepts and companies, but it was a kind of hard to find anything which made you say "this has the magic touch and has never seen before".

I know this is a difficult statement because it can be interpreted as "bad quality ideas and start-ups", so let me underpin that it's not the case. But I think it is a sign for where we are in the current cycle which is waiting to see which premises are right and which are wrong. To provide some perspective on this: In our daily consulting practice we like to think along the question of bottleneck factors for competitive advantage in crowded spaces, and start-ups are crowded today with all the implications for angel investment.

Therefore a cool thing was a med-tech start-up

As such it was refreshing to be pitched by a non-web-star-up Anaconda from the med tech sector. They are trying to improve stroke treatment and their pitch was as valid as the pitch of many web start-ups (you can find an interview here). Also it is again a confirmation that opportunity is not in web technology only.

Now I want to focus - as with the previous two articles about the Web Summit - on startups in particular from sectors where we are serving our clients.

What about Software as a Service after Web Summit

The first sector is software as a service. For a snapshot and numbers about participating SaaS look here but I think it's noteworthy to report some general impressions here.

The first one is that European SaaS is starting to really move. Around the Web Summit I interviewed Accel partner Phillipe Botteri about the state of European SaaS. He stated that SaaS in Europe is getting more interesting and gaining momentum. This was a nice confirmation of our observations of the European and in particular German SaaS market.

A different breed of SaaS solutions arises

Then I think it is very interesting to take a look at the problems and business models the SaaS companies are solving.

The most interesting contrast derives from a comparison of what you see on average in presentations in Germany (as well as in Italy and Austria) about SaaS. Most of them tell you about the enterprise legacy software disruption by SaaS which already should have happened by now. This in turn should mean that theses spaces are already long filled. But talking to SaaS startups and checking the exhibition list provides a different picture.

With this background you find that the most prominent startup in the SaaS category is a solution to relive the pain of project management. This strikes me in particular – although Wrike is an established startup founded in 2006 (beta in 2007) - as I longtime argue that the first wave of SaaS companies did primarily port processes from legacy software into the cloud, not necessarily innovation in the process space. As such and with Wrike still being hot it might be too early to say that we have already seen the winners in enterprise resource planning and related tasks solutions. For example my office and many colleagues I know are still not satisfied with the various project and task management SaaS solutions out there.

One SaaS start up that stood out is SpazioDati, I have also been mentioning in the first article. They are one of 3 million plus startups with the SaaS label and the only European representative in that sector (according to the Web Summit labeling). They offer an interesting semantic analytics solution based on hard science.

For a snapshot I took an interview with the founder and cofounder Michele Barbiera you will find upcoming on our blog.

In order to provide a wider window into the current SaaS state I also talked to Meeting Mole, a German SaaS startup which is in the starting phase planning to improve B2B sales. Talking about their challenges an old thesis of us was again confirmed. SaaS sales U.S. and SaaS sales EU are very different.

With this to Enroron, an industry specific work process management solution. This seems to be as close as we get in Europe to Vertical SaaS at the moment. Noteworthy here the implications of Windows 10 for their solution.

Another thing that that is interesting to observe talking about SaaS startups on Web Summit is the fact that besides the classic analytics, tracking and metrics we now see solutions emerging that offer solutions to SaaS and online companies themselves. Algolia, a startup trying to solve the problem of searching within websites (mainly ecommerce) is an example of the latter one. And its solution operates way outside the usual SaaS narrative.

Of course there have been many more, and probably one solution overlooked. But I think the exemplary listing shows the variety and reality of SaaS in Europe compared to trend Power Points about SaaS pretty well.

This closes part one of this year's Web Summit review. The next part will include Fintech, IoT and a final assessment.

What sticks four weeks after the event is best described as a strange mix of "being overwhelmed by information" and "nothing new". It does not mean it was no great event. It was, but the above impression remains. This result is a confirmation of Iceventure's current view of the innovation and startup ecosystem in Europe which is moving more in the later stage of the cycle.

What sticks four weeks after the event is best described as a strange mix of "being overwhelmed by information" and "nothing new". It does not mean it was no great event. It was, but the above impression remains. This result is a confirmation of Iceventure's current view of the innovation and startup ecosystem in Europe which is moving more in the later stage of the cycle.

Schreibe einen Kommentar

Achten Sie darauf, die erforderlichen Informationen einzugeben (mit Stern * gekennzeichnet).

HTML-Code ist nicht erlaubt.