As money transfer is about trust and legal transactions you have to make sure to either identify your users and their transactions or/and have pretty high tech fraud prevention algos running. PayPal started with email (sufficient) and added other means around. Thus, I argue that starting with the tax number is a pretty good case of identity clearance and therefore trust generation.

Of course, we can debate the nuances of trust in the case of the Greek government and its tax authorities. You will however agree that the identity of participants for transactions secured by the tax number and the fact that amounts transferred could have been partially covered by tax debits/credits function as a good safety net.

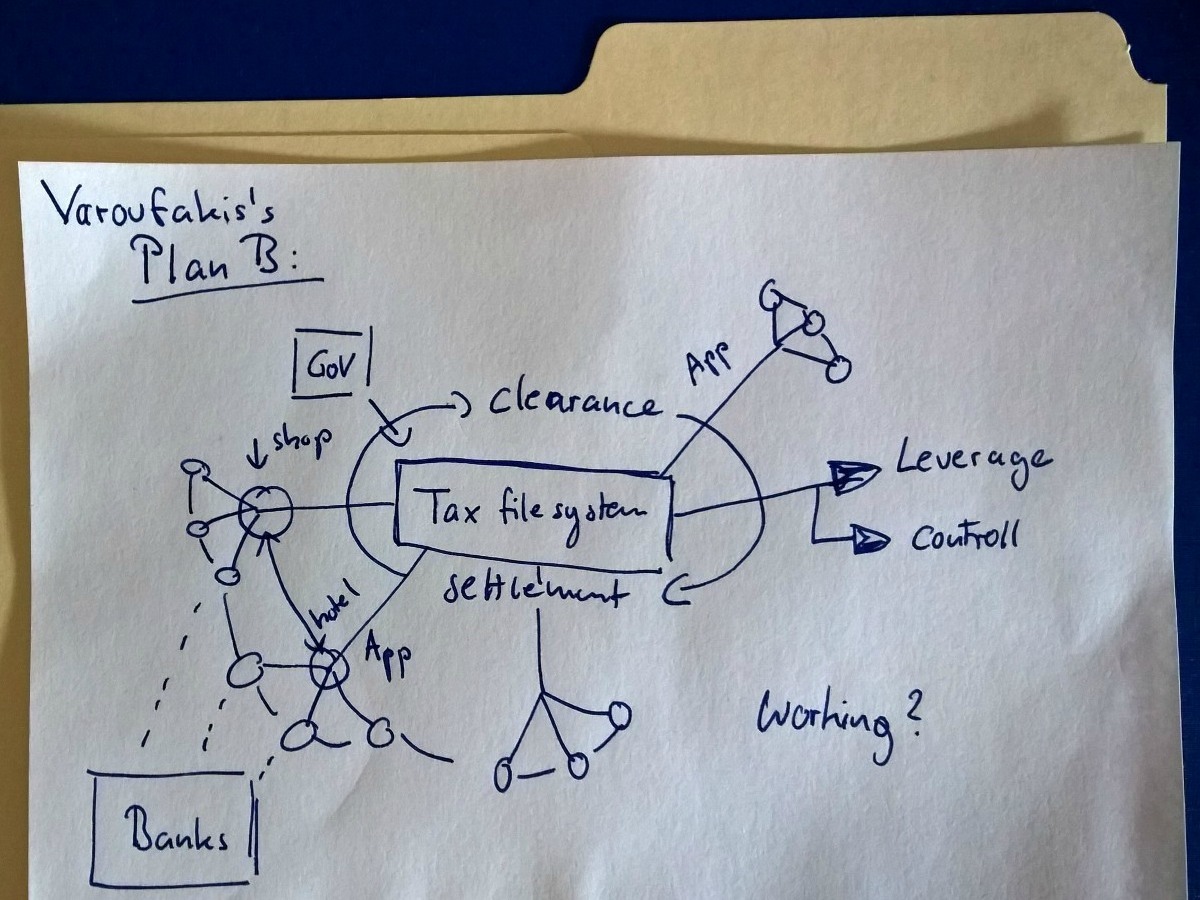

The second aspect of safety is the correct recording of all transactions. As this is expected from tax records, it seems to be the reason to start with the tax software. The adding of records of +/- to an existing ledger appears to be feasible.

Key take away for Fintech startups: Check if you can build your business case around established complementary organizations providing proven identities.

2. User base & capitalization in Plan B and Fintech start-ups

Point 2 examines the critical numbers of users to be an effective payment system and not the last used option. As slick as your codebase and UI might be, a disruptive Fintech start-up needs users and network effects. Concerning this aspect, all (potential) taxpayers of a country hooked up onto your system is not too bad as a user base to start your payment service as in Plan B and most likely guarantees that everybody uses it.

Then the system needs capitalization = liquidity, meaning a resonable volume to cover costs. The payment system in Plan B could have been quickly capitalized when the Greek government would have transferred the next round of wages and pensions on the tax number account as well as other payment obligations. There is no simpler reason to get people to use it then. This turns it into an alternative to the banks and could have provided sufficient liquidity for the economy (see point 5 and 6). Prof. Sinn argues in the same direction. It is likely to argue that Greek companies would have been oblarged to do the same, turning away from the banks.

Lesson learned is that a Fintech startup should consider a cooperation strategy with a wide and existing user base and a reason for payments with your system. Compare it to the symbiosis of PayPal and EBay. Together they generated the trust and their user base.

3. Roll-out and scaling

This point is a bit more for underpinning the argument in its completeness as the tax authorities in Greek seemingly already had a software, internal accounts and web access to it, but it still offers lots food for thought for start-ups.

Once you have a website with your system in the background (the tax authority software) running, there is probably less concern that it cannot scale. But you have to make sure that as many people as possible can use it everywhere. It also as to work for companies and you need the human resources to process the data. Therefore the leaked Plan included an app, of course also debated.

Availability and working everywhere by an app

How difficult is it with the system up and running to complement it with an app? What would this app need: In the first version nothing else than a login, a simple form to type in your ID and the receivers ID and the amount in transfer. Additionally a transaction confirmation (+ maybe a database for control). Does not sound like overly complicated for programmers.

Now the distribution: 10 million downloads of an app in 24h-48h (e.g. over the weekend) does not sound as an unsolvable problem today from the technical side with services like AWS around. The social scaling to all users is in the case of Greece simply done by an emergency law. This is what (political) disruption in crisis really means. You go from A to B with one signature.

The psycologial side of adaption

Concluding, it is more interesting is to think about the sociological aspects than of the alleged "impossible" introduction (read more on the time aspect below – point 5 leverage).

Sure, the introduction in Greece under the circumstances would have been a shock which can be mitigated by a working system. So you want to check for working user cases: What percentage of smartphone diffusion does the Greek population show? Is it evenly distributed through all age groups? What could be the next class of device your population could adapt to in case the number one device is not smartphones to have the system working everywhere? I think an internet-connected computer and printer per shop is enough. It also provides a solution for tourists. This could also work as a pay-in counter. Sometimes it is about simple solutions, too. This are interesting points to consider for any start-up thinking about their first adopters and scaling.

Additionally there is another interesting piece of psychology you can observe. Many journalists wrote that such a system would never have worked as people need and want cash e.g. for the supermarket. But - that is just one preference amplified in the crisis.

In general, people like cash because it allows a more controlled (form the user's perspective) and uncontrolled (you are more difficult to track) spending usage vs. user's convenience and risk preference (the old macro money velocity formula). That is why we use cards. In the particular case of Greece, the want for cash came out of two fears: A breakdown of the banks and an assumed shift to Drachma. Here it makes sense to hold as much Euros at home as possible as Euros are not in control of your (upcoming) central bank and out of your, to be bailed-in bank account.

Still it does not make a case against the alternative payment system of this Plan B, simply paying with the app of it at the supermarket cash register. As such, the generalized statement is less a fixed preference than an expression of switching costs in terms of money and time in a society with established payment means or - in crisis - of other concerns. I found it another great example of the fallacies of perceived (Fin)tech aversion (often told in Germany) that fails to identify the tipping point in convenience of existing systems and not in the refusal of technical solutions.

The user case for b2b

Still the case for companies is open where the amount of transaction data is significantly higher. Here an app is no solution. I think that this was the real challenge in preparation, but probably solvable. The reasoning is that I assume that companies already exchange more data with the existing platform of the tax authority such that the API was there and only to be extended with code.

A thought about team size for Plan B and in Fintech

There is a second aspect of scaling - theteam. Plan B started with 5 people, like in a start-up. How many people are then necessary to run operations? Equens the largest EU provider employs about 1500 people for EU wide payments comapred to about 11 Mio. Greeks. Concluding, it depended most likely only on the quality of the preparation of the system in the 6th month time frame as there are enough government employees you can put to work later.

The key takeaway for startups is how to identify the transformation moment that turns the perceived impossible into the new normal. Concerning plan B it would have been an extreme negative event. What could be a positive analogy for a Fintech start-up?

Another lesson is the timeless reminder that your business case works best in case of urgent need with you providing the solution. Maybe some Greek start-ups should still look into the case.

4. Settlement 2.0 once you have clearing house and commodity feature like means of exchange

With point 1-3 you already have a functioning payment provider in place. I wrap up: You have identified customers (security), they can use the system (almost) everywhere, you track transactions, people get quick to the solution, all is electronic and in case of Plan B and the circumstances design features and other convenience features needed for attracting customers are of second order importance. Nevertheless, this is not enough for Plan B.

For that we first have to name one of the root cause of payment problems in our modern financial system architecture. It is the double function of money as means of payment and means of investments (for the bank) in a normal account. I think a solution around it is one of the most interesting parts in the plan B and for all start-ups in the sector of financial technology.

I therefore beg to argue that a transaction mechanism is not the most difficult part. It is the settlement/storage and the difficulties around it. By that, I do not only mean the legend and balancing of accounts. I refer to the part of conversion into real money when people take money out of the system (think about the implications for your margin/business model). PayPal has to do it; a payment startup has to do it and Plan B, too. And there are many good reasons for it. Other payment obligations for example, cash for everyday transactions, but most of all it is safety. Unless you are a trusted bank, people want to have the money on their account there. So either you are a bank (with CBs as lender of last ressort), or - for improving trust - you have to have a large balance sheet. I think this is still one of the biggest adaption hurdles for Fintech innovation and a reason why banks might prevail for long. Thinking about the Fintech enthusiasm and the narrative of "being overbanked" in the 1st world it is interesting to see what will be the outcome. For the full context of the problem we still have to be aware that a trusted bank will have to use the money as "deposit" for their credit business. This is where liquidity issues arise from. This was exactly the situation in Greece.

With that background information back to Plan B. Remind that the payment system had to play a kind of liqudity provider to the economy in order be a real alternative. Normally a government could provide this deep balance sheet. But what to do in a situation where you as the government are short of money, banks are at risk and the payment system takes more the role of a monetary supplier? Your plan needs to cover this aspect too - enough liquidity circulating if only electronically to not worsen the systemic crisis – until you can payout cash. I leave aside the legal issues like if you could run it out of a Ministry or better set-up a clean company structure with usage rights for the software. But you could have done it technically, which is expained in the following.

My general argument as answer to the above-sketched problem is that - as in the solution by Plan B - real Fintech innovation cannot and should not only resemble the old banking structures, but also add something to the systemic architecture. That makes it a game changer.

What sets Plan B apart from normal payment system providers

With that background thought it is to explain that a very intriguing feature of plan B was the additional settlement opportunity stemming from two features – the data availability of such a centralized system and a second means of exchange besides the e.g. pension transfer via the use of tax credits/debit. Thus, the settlement quality of Plan B refers to not only accounts and ledgers, but to a kind of clearing house position, the tax authority takes with such a setup, which allows for netting. This is for the fact as outlined above that you have data and almost every transaction has a tax contribution part, which often is running through many books until the final payer is defined. This means risk of default at each single player on the amount of transaction and the tax part which now is better taken care of. In addition the nature of a tax claim/credit provides it with commodity like features that can be leveraged as I will explain in point 5.

The point illustrated with the example of invoices over a b2b Fintech platform

As this is very abstract, consider the following real life example for b2b transactions, Tradeshift, a great Fintech start-up providing digital invoicing as their basic layer service. In this blog post I explain all aspects in detail. For this post it is enough to know that your startup solves the problem (and has unicorn potential) and solves the problem when

a) there is a rich basic data layer from the payment process itself - the services and goods named in the invoice (+ plus the fright papers)

b) a commodity-feature of the whole underlying economic transaction like a backed obligation - meaning the cash claim comming from the invoice

c) you can separate the payment function from the investment function of traditional financial service providers as it introduces a new systemic option.

d) and offer an alternative solution providing liqudity based on this

Tradeshift combines them all via the document business layer, meaning the invoice, which is nothing else than a goods or service backed YOM (you owe me). It has therefore all the fundaments for the oldest form of merchant banking - lending against documents - and again clearing.

An explanation in short of the advantages: We prefer to settle invoices with cash (or a debit), but it is not necessary as we could settle with other goods and services in exchange. In complex value chains (or in a country), the relationships are very often overlapping. In such a situation, a clearing house with all data, albeit a concept for financial market transactions, also in case of payments diminishes the need of cash in the system while allowing for many transactions with a similar risk level. Plus you can help all players on the network to work together with financing and discounts.

With this real life example of supply chain financing, back to the more abstract level: Plan B could have allowed the usage of tax debit/credit for payments and a distribution of funds from strong players to cover their chain's financial needs. I argue that a tax credit/debit has a similar strong claim as an invoice if not stronger (I do not know about Greek insolvency/bankrupt law but assume that government claims like taxes a senior). Thus the approach in Plan B was right because it was not only a means for decoupling from the banks, but had an alternative means of exchange to cash of value for all and the data to take allocation decisions that are data and market driven.

In conclusion, when your plan is to create something really disruptive in Fintech, make sure your market shows similar signs. For the argument, another thought for Fintech startups: what do you think is the adoption channel? Is it c2c then spilling over to businesses or is it b2b? While the question sounds trivial, there is a lot of margin distribution and real need embedded in and that is while I argued it is for b2b.

5. Leverage for enough liquidity and money supply

A starting thought - all magic in finance is about leverage especially if the Fintech start-up is in payment or credit. While it provides income and low equity systemically it is part of the money supply. Therefore, point 6 is the logical continuation of point 5. That is also, why the payment functionality of Bitcoins is great, but the banking and alternative currency story is just not working from a macroeconomic view, as (the right) leverage is important for an economy.

As such, Plan B in my point of view especially had to cover this aspect, at least to some reasonable degree, as it would have been the only liquidity provider to the economy (albeit in electronic form) with all banks shut. It could have/did. First, there is the reduction of cash needed due to your clearing house function. Second, the ingenious aspect of the tax number for a payment system is, that it is very simple to add some leverage into this set-up due to the data set, which allows for good risk controlled leverage. You have good data and you are the government. So why should you not allow people in the system to spend more tax credit/debit besides the direct capitalization even if only electonically?

A bit speculative, but I guess a plausible reason to talk to hedge funds was to see if they would finance a tranche of that leverage if even only for optics. While it remains a big question if you could run you Plan B based entirely on Euro base for a longer time, I think it is plausible to have had a sufficient enough liquid and working payment system giving the time to distribute money in cash again.

An important aspect is of course as with all credit how to prevent fraud. E.g., how can one avoid a case where someone uses all the tax credit on a made-up service and then defaults? The risk compared to normal times is to not only loose taxes, but the additional amount, too.

This one is tricky, but as we are operating under special circumstances, a realistic solution is to allow for the leverage based on tax records (meaning you know the average declared income/revenue/costs) and live with some fraud. The question in my opinion is more if the setup of the payment system is systemically weak to have more adverse selection than in other cases.

Secondly, the rule setting in such circumstances and system is simply following a hierarchy of most important social needs, while special cases could be dealt with passing by the office and showing a detailed documentation for the needed transaction and a higher tax credit/debit.

The lesson for a Fintech start-up is that when your clients or data set allows introducing leverage you are in. Start with a solution via API if you do not want to take the credit risk, but think of adding your own risk taking. But beware, financing and leverage has two natural enemies. Years ago, I was involved in a project examining if you could venture capitalize new financial institutions or services as the higher equity valuation ideally can be engineered naturally in such a case. On paper, it works but finding quality financing objects and avoiding adverse selection are issues in the real world. These very endogenous facts of the Fintech business – as long it is not pure IT provision – have to be hard thought of in your business plan.

6. Extra service layers of Plan B for Greece gov and ideas for start-ups

Sometimes I wonder why Fintech start-ups do not think more often about additional services for the user. I mean, in the end the quest for innovation is about tech and offering a better user experience.

This sounds strange introduction concerning Mr. Varoufakis's plan, but there was a new service layer. The additional service – correctly it is a benefit for the operator – in Plan B is a better, if not full, control of tax payments. Almost all transactions in Western societies involve some tax amount and now you proceed them with your system.

Thus, actually all – especially the creditors - should have cheered such a solution (despite Greek citizen's maybe) even afterwards as it could help to solve the officially biggest issue of the Greek crisis –tax evasion, too. Thus, I argue it is still a great idea to look for solutions in this direction with banks in trouble, the need of a structural fresh air reform, catch-up with digitalization and a tax evasion problem. An example of a Fintech/ebilling b2b platform fostering this change is described here. Maybe Greece wants to look at.

Of course, that is a very special case. Still I deem it interesting for Fintech start-ups to think of additional services especially for SMEs. Monthly (VAT) tax preparation (reference is to Germany) is still painful and takes time. Moreover, as an example, why not give each of your users a kind of email address? The invoice data and bank information is simply mailed to it and transferred into the system. The payer just has to check and confirm the submitted data. This would be a service improvement and knowing that the idea is now 14 year old makes me wonder about all this service disruption.

Concluding two apsects should be clear now:

I am not an expert of Greek law, but most international/German commentators are most likely neither. As such, there is no valuation about the so "called" hacking. I simply think it showed how desperate the situation is/was and I am more astound how less reflection is about this fact about its real implication for all of the Eurozone. We are in a secular change as I continue to argue, which will affect the North, too.

Then it seems absurd to first attack Varoufakis that there was no Plan B and then again that there was a Plan B. Every good manager, if start-up or not, should prepare alternatives (and do so in silence) for different outcomes. Desperate situations breed desperate measures.

Then, Plan B was an ingenious approach to establish a working alternative payment system most likely with enough liquidity for the Greek economy given the circumstances. The plan covered most if not any aspect you will think of when trying to introduce a payment service e.g. by founding a Fintech start-up in this sector. The bar was even higher: This one had to work for a whole population and as a kind monetary supplier, too. I think we should also take path dependency into account. Once introduced it is the new path. As such it could have been succesfull if only performing above avergae of the expectations.

It is not to say that it would have solved the Greek debt problem or worked to run over long time with Euros without additional support. But it could have worked as a solution and introduced some interesting side aspects, still important for structural reforms in Greece today.

As such, it was not the payment functionality, but the fear of a shift to Drachma that could have resulted that created the outcry in Greece (and among Euro pros).

Secondly, the gap between "the possible" thanks to technology and the perceived "impossible" made visible with the various media reports about Plan B demonstrate the cognitive dissonance about the real situation and possibilities, the opportunity to disrupt as well as the dangers – especially in Fintech – to do it too fast. I argue that this is a confirmation for the b2b adoption fist, again.

Last, as we are still experiencing a full-blown government debt and banking crisis, it might not be your Fintech innovation, but your courage to deliver a solution in total uncertainty that is the foundation of a tomorrow's Fintech multi billion business. Therefore, I recommend governments to work on solutions with the private sector that can help to bridge systemic problems like "banks too big to fail".

If so, as I discussed throughout 2014 and this year, you might want to think twice and harder which implicit assumptions on society you want to found or finance. Tomorrows needs and solutions might just be very different from today's ones in our debt fueled world.

Update and Editing: Since publication I added some explaining phrases for non-sector readers. Point 6 (now) was former point 4. I also added the background links. - 11.08.2015

Background material:

The leaked tape with the Plan B - http://www.omfif.org/media/1067578/omfif-telephone-briefing-greece-and-europe-after-the-brussels-debt-agreement-yanis-varoufakis-16-july.mp4Features of new payment products. Albeit partialy a company PR, still a nice list from a professional - http://www.paymentsnews.com/2010/04/the-nine-characteristics-of-successful-new-payment-products.html

3 Kommentare

There are several interesting things in this article.

Good article, thanks and we want more!

WONDERFUL Post.thanks for share.more wait

It’s hard to find educated people on this topic, however you sound like do you know what you’re discussing!

Thanks

Schreibe einen Kommentar

Achten Sie darauf, die erforderlichen Informationen einzugeben (mit Stern * gekennzeichnet).

HTML-Code ist nicht erlaubt.